Last year CNN asked “What if Companies Issued their own Currency” where printed money bore the images of corporate celebrities instead of George Washington or European landmarks. Although neither George Orwell or Aldous Huxley’s dystopian futures predicted a world governed by corporations as opposed to authoritarian governments, it may be more plausible to imagine a world where corporations control the money supply, not with coins and bills but cryptocurrencies. In fact, the fad amongst many technologists today is to encourage the disintermediation (or deregulation) of money by moving to Blockchain-based cryptocurrencies like Bitcoin. But instead of removing the middleman, we are more likely – contrary to the idealists’ ambitions — to open the door to empower big tech companies like Amazon, Facebook and Google to tokenize their platforms, replacing one currency regulator with corporate ones. Let me explain.

At the beginning of the year, the encrypted messaging system Telegram announced plans to issue its own cryptocurrency. Telegram’s vision was to create its own Blockchain-based cryptocurrency around its chat-service where its users could engage in all sorts of transactions and make payments through Telegram’s own digital platform. By leveraging the mass hysteria around Bitcoin, Telegram hoped to raise tens of billions of dollars in financing from its ICO.

An ICO (or Initial Coin Offering) is the process of raising capital through the use of cryptocurrencies, instead of issuing debt or equity. For those new to the concept, cryptocurrencies (to paraphrase Wikipedia) are digital assets designed to work as a medium of exchange (generally through a Blockchain) that use cryptography to secure transactions, control the creation of additional units (ie, the monetary supply) and verify the transfer of assets.

Think of cryptocurrencies as those tokens at a video arcade where in exchange for hard currency (or services), you are given tokens that can be used at the arcade. The tokens would generally have no value outside of the arcade, unless there is demand for exchanging goods, services, or other currencies for those tokens.

Think of cryptocurrencies as those tokens at a video arcade where in exchange for hard currency (or services), you are given tokens that can be used at the arcade. The tokens would generally have no value outside of the arcade, unless there is demand for exchanging goods, services, or other currencies for those tokens.

With an ICO, an investor acquires those tokens, which may be either the issuer’s own (often newly) minted token or another existing one like Bitcoin or Ether. As mentioned, the tokens acquired through the ICO are not debt or equity. They are digital claims to future rewards or services. Investors acquire the tokens in expectation that there will be a dynamic market to buy, sell, or transact using those tokens. Because the tokens are exchanged on a Blockchain, each transaction is logged and permanently traceable (though encrypted). In theory, an ICO is more cost effective than a traditional securities offering because it does not require the efforts of a VC or financial institution and is not regulated.

Well, we thought ICOs were not regulated. According to the Wall Street Journal, a number of companies that issued ICOs are currently being investigated by the US Securities and Exchange Commission.

The sweeping probe significantly ratchets up the regulatory pressure on the multibillion-dollar U.S. market for raising funds in cryptocurrencies. It follows a series of warning shots from the top U.S. securities regulator suggesting that many token sales, or initial coin offerings, may be violating securities laws.

One might cynically say that regulators are predisposed to dislike cryptocurrencies because they cannot control them. On the other hand, if ICOs are not regulated, then there will always be a risk to the consumer, something that the 1933 and ’34 Securities Acts were designed to address with significant success over the past century. As mentioned in the article:

Many of the coin offerings happen outside the regulatory framework designed to protect investors. Hype around last year’s bitcoin bubble led to many cryptocurrency offerings for startup projects. Some of them had little, if any, basis in proven technologies or products, and many were being run outside the U.S. In some cases, investors caught up in schemes that turn out to be fraudulent may have little hope of recovering their money.

A soon-to-be published Massachusetts Institute of Technology study of the ICO market estimates that $270 million to $317 million of the money raised by coin offerings has “likely gone to fraud or scams,” said Christian Catalini, an MIT professor.

Overall, there are a number of reasons for dealing in cryptocurrencies:

- To incentivize developers/computer owners (aka, miners) to verify transactions on the Blockchain and support and maintain the platform

- Financing of start-ups (ICOs)

- To bring more transactions to a platform

- To engage in unregulated transactions (ie, black money)

- Speculation

As mentioned, companies like Telegram and many technologists (even some investors) may also find the use of a cryptocurrencies attractive because they have largely been outside of the control of governments and regulators. But this raises the question about whether fiat money is actually more stable than cryptocurrencies and therefore in the long run better suited for investors and society. One of the foremost concerns of any investor is that she has a viable exit, meaning that she is investing in a liquid market where she can put in and take out her money easily. So the question is whether a cryptocurrency can give the same stability that a government-backed currency can.

When you start thinking about Telegram creating its own private market of tokens for transactions through its chat platform, remember going to the video arcade to play PacMan and having to convert your money into tokens. Now imagine a future where Amazon does the same thing. It issues its tokens that become the only currency available for transactions on amazon.com. Then imagine trying to download apps, stream music, movies or other content on your Apple devices and having to use Apple tokens. Maybe each major platform will have its own tokens, and its developers and maintenance crews (aka miners) will get paid in their employer’s respective cryptocurrency. Workers will only be able to spend their hard earned salary at the company store. We can call it the digital hacienda or crypto-feudalism. Welcome to the new crypto-world order.

When you were a kid at the arcade you had no problem spending all of your tokens at once before your parents dragged you home. But as an adult, if you have your money tied up in Amazon tokens, WeChat tokens, or Facebook tokens, what happens when that company goes bankrupt? Or what is the conversion rate from one token to the other? Wasn’t the advantage of using US greenbacks that they were backed by the U.S. Fed, were easily exchangeable and that US government wouldn’t go under? Will these companies have to create their own monetary departments to control the supply of their tokens, and fight against inflation? In other words, instead of removing the role of central banks, companies would become central banks themselves. In fact, the more I read about cryptocurrencies, the more the macroeconomic fundamentals behind hard currencies makes sense. Or I am just old fashioned?

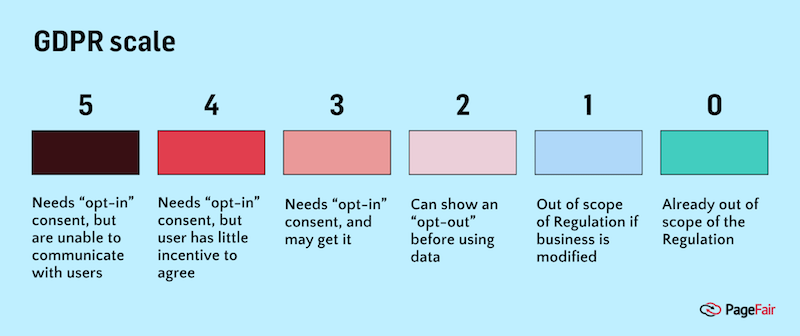

Have you noticed that you’re now receiving dozens of emails from all sorts of services that you forget you ever used? Everyone is suddenly sending you requests to accept their new privacy terms. Yes, that’s the imminent arrival of the EU’s new General Data Protection Regulation, due out in stores on May 25, 2018, talking to you. So if you’re feeling like the prettiest one at the dance or the most popular kid at school, then you have the GDPR to thank (along with its threat of massive fines).

Have you noticed that you’re now receiving dozens of emails from all sorts of services that you forget you ever used? Everyone is suddenly sending you requests to accept their new privacy terms. Yes, that’s the imminent arrival of the EU’s new General Data Protection Regulation, due out in stores on May 25, 2018, talking to you. So if you’re feeling like the prettiest one at the dance or the most popular kid at school, then you have the GDPR to thank (along with its threat of massive fines).

The more I hear Blockchain evangelists preach about tokenization and how cryptocurrencies will democratize technology, the more I am convinced that cryptocurrencies are one big swindle. I have already discussed this more in depth

The more I hear Blockchain evangelists preach about tokenization and how cryptocurrencies will democratize technology, the more I am convinced that cryptocurrencies are one big swindle. I have already discussed this more in depth

We keep hearing that governments will kill cryptocurrencies or at least regulate them to death. They fear what they cannot control (or tax). I tend to keep a more open mind.

We keep hearing that governments will kill cryptocurrencies or at least regulate them to death. They fear what they cannot control (or tax). I tend to keep a more open mind.